Category Innovation Down

As the Covid-19 pandemic continues many households have changed their shopping behavior to cope with the situation. We already showed that shoppers shop less often but spend more on each occasion. But what about supplier activities? Today we examine innovation.

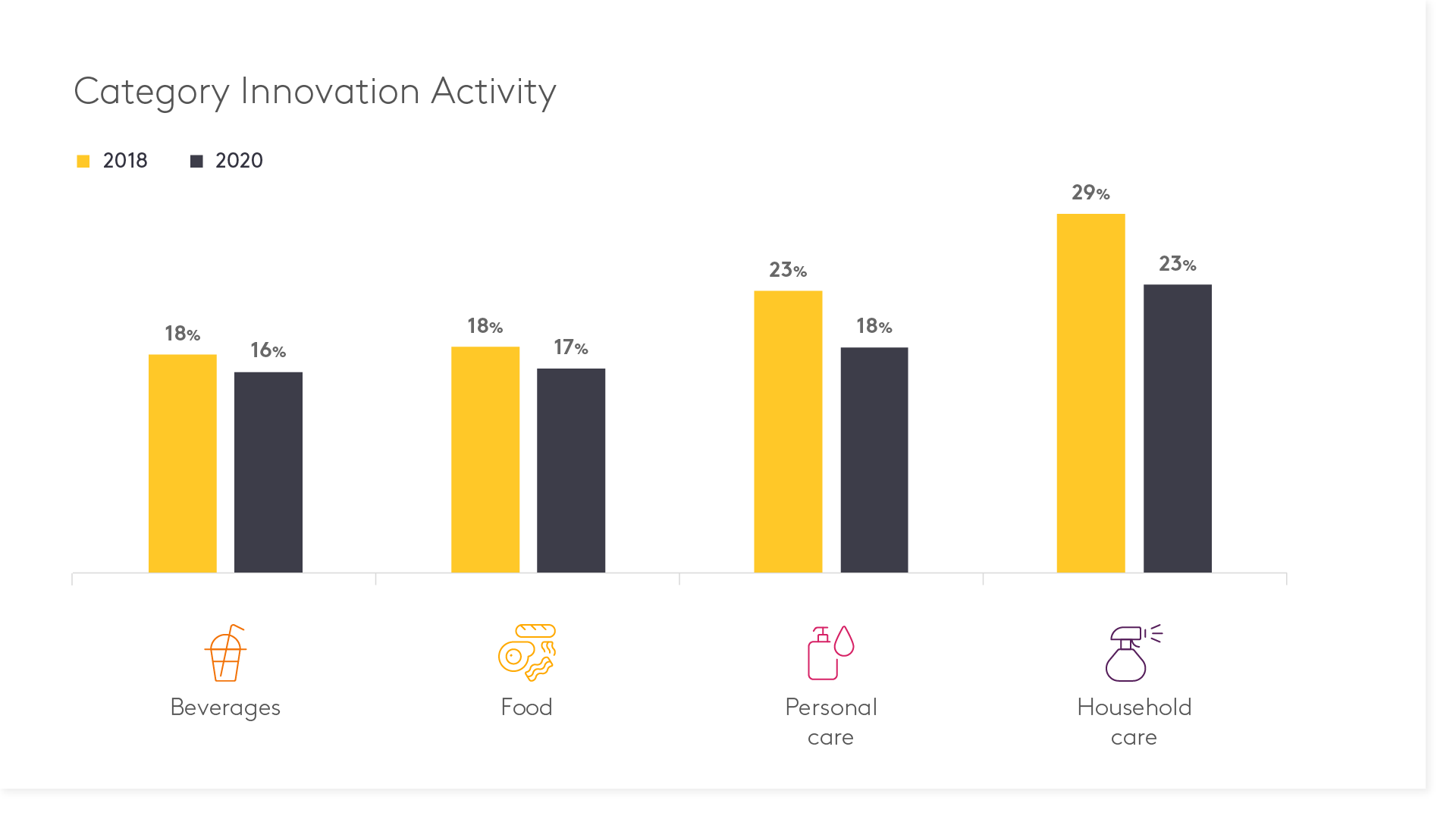

We compare innovation activity in 2018 with 2020 for 8 countries in Europe and Asia and across more than 700 categories. We define innovation activity as the number of new launches in a category as a percentage of the total assortment of the category in that year. This is what we find:

- On average, we find a large drop in innovation activity: New product launches accounted for 21% of the average category assortment in 2018, a number which declined to 18% in 2020.

- Household care and personal care show the largest decline (-6 and -5% respectively), followed by beverages (-2%), and food (-1%).

- While many categories see their innovation activity decline, we find selected categories that actually increase the share of new products within the category assortment.

- Many of these categories are staple categories – like canned beans, canned fish, mineral water, instant coffee, packet soup, or personal care products such as hairsprays, toothbrushes, and soaps.

It is understandable that companies try to find ways to reduce marketing investments like new product activity in challenging times. However, this is not a sustainable strategy as many of our past blogs have shown: Investing in recessionary periods pays off because (a) it offers more bang for the buck given limited spend by a majority of companies and (b) it is a necessary investment to stop private labels growing disproportionately in recessions. Looking ahead, preliminary analyses of 2021 data indicate that the number of launches have dropped further in 2021.

Data: More than 700 categories in Austria, Belgium, Hungary, Italy, Netherlands, Poland, Romania, Spain, Data on Launches and Category Assortment Width 2018 and 2020