Growth 2019-2023

Some more learnings on what distinguishes winners from losers in this high-inflation and Covid-19-impacted period

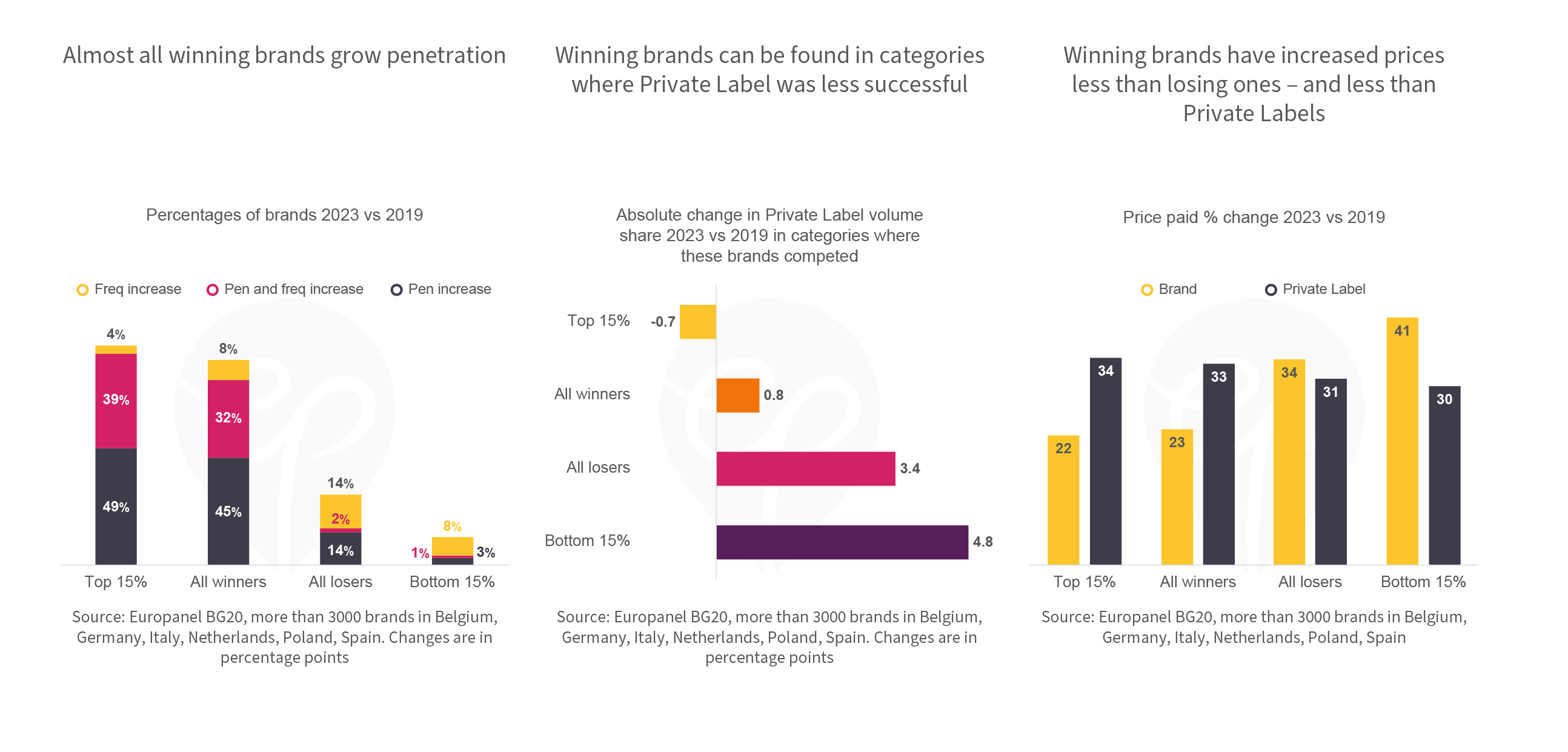

Almost all winning brands grow penetration

Among brands that gained vs lost share from 2019 to 2023 we see that almost all winners increased reach (88% among the top 15% and 77% among other share winners) while hardly any share-losing brands grew their buyer base. Less than half of all winning brands also grew frequency – but keep in mind that we saw a decline in the average category purchase frequency throughout that period.

Winning brands can be found in categories where Private Label was less successful

Private Label share gains have been substantial between 2019 and 2023 with the average category seeing Private Label share increase by 2.2 percentage points. In categories where the 15% top winning brands compete Private Labels on average have actually lost share – highlighting that (a) Private Label share gains are not a law of nature and (b) successful brands can win back share. Brands with the biggest share drops find themselves in categories where Private Label has gained strongly – on average 4.8% over four years.

Winning brands have increased prices less than losing ones – and less than Private Labels

We showed last week that winning brands decreased their promotional activity, but less than losing brands. In terms of price paid changes overall, they experienced substantially smaller price increases (still a lot given the levels of inflation over the past couple of years): during the past four years prices of winning brands went up by just over 20% while losing brands increased prices by more than 30%. These numbers are noteworthy because they compare favorably (or not) to changes in prices charged by Private Labels: winners increased prices less and losers more.