Brand Price Premium not related to Private Label Success

Private Label (PL) success in a category is often linked to price in contradictory theories: (1) A large price gap between brands and PL provides potential savings and motivates people to switch to PL. (2) A small price gap between brands and PL suggests a lack of differentiation and motivates people to switch from the ‘bland’ brand to PL.

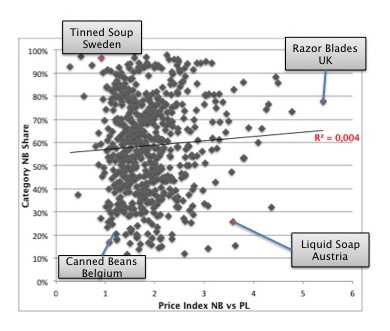

Actual purchasing evidence does not support either of these arguments: Across eight hundred categories in 12 European markets we find all combinations of price premiums and PL success: High premiums with low as well as high PL shares, low premiums and again low and high PL shares. In statistical speak: The correlation is 0 – meaning there is no detectable relationship between brand price premium and PL success. However, this does not imply that individual brands shouldn’t take care in pricing versus PL.