Shopping frequency is back to ‘normal’ and shopping around has resumed as Discounters return to share growth.

And which channels are most impacted by that return to growth and renewed shopping around?

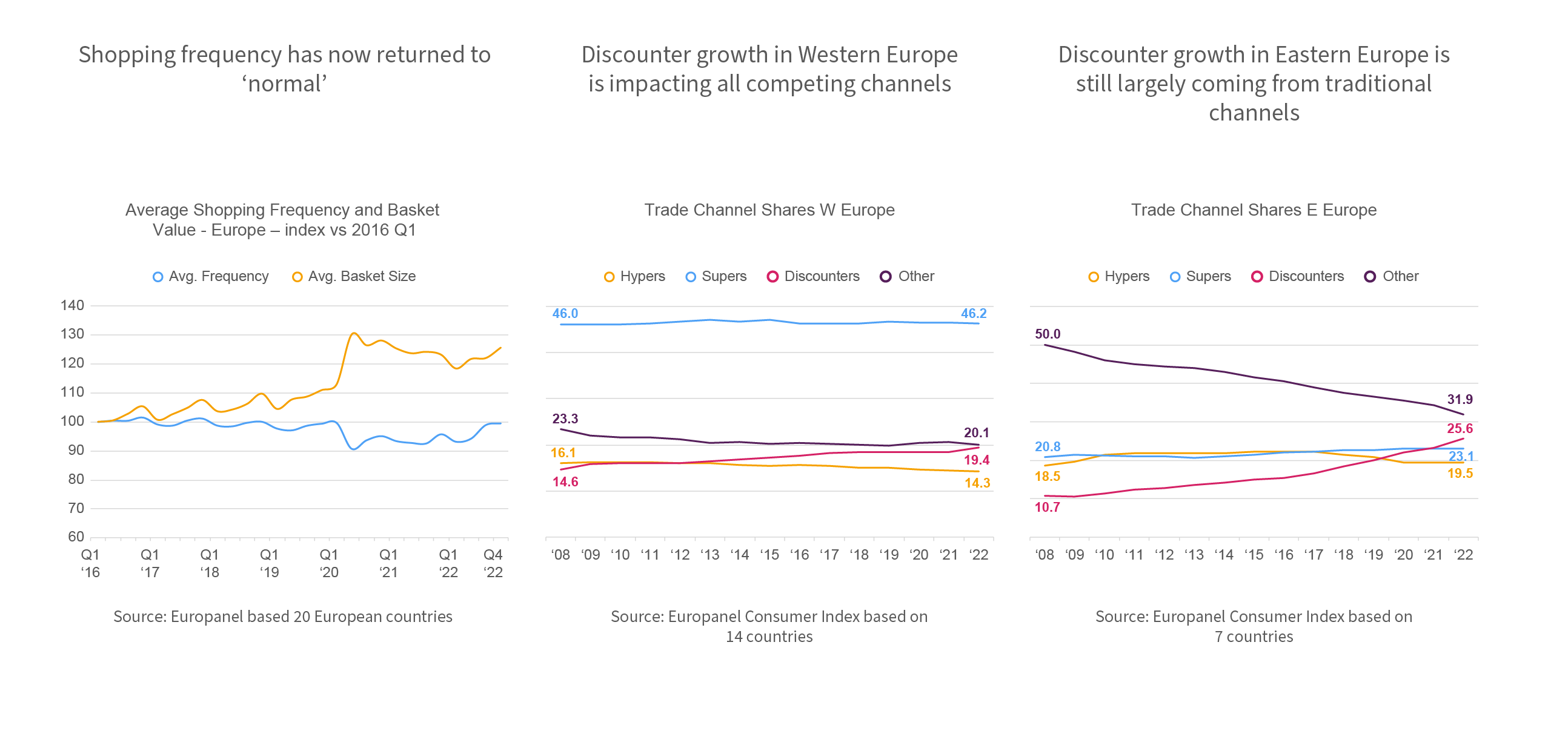

Shopping frequency has now returned to ‘normal’

The pandemic meant less shopping around, fewer store visits and very large basket sizes in a record FMCG market. The rise in Discounters and inflation in 2022 have led to more frequent shopping trips again although basket value remains very high due to the rise in prices

Discounter growth in Western Europe is impacting all competing channels

For some years Hypermarkets in Western Europe have been losing share. This has been driven both by the rise of online, especially in the last couple of years, and also by the return to growth for Discounters, driven by store numbers and appeal. Supermarkets and online have also been impacted recently by the renewed Discounter growth.

Discounter growth in Eastern Europe is still largely coming from traditional channels

In the long term there has been a continuous decline in Traditional Channel shares in Eastern Europe. This trend remained in 2022 and it is largely from these stores that Discounters are gaining although there are also signs of an impact on Hypers and Supers now.