This week we concentrate on the grocery market in Ukraine

Our GfK colleagues there have been resisting and continuing operations in agreement with panel members. We can now share the latest trends covering like-for-like regions. Our best wishes continue to go out to our team, our panellists, their families and everyone there.

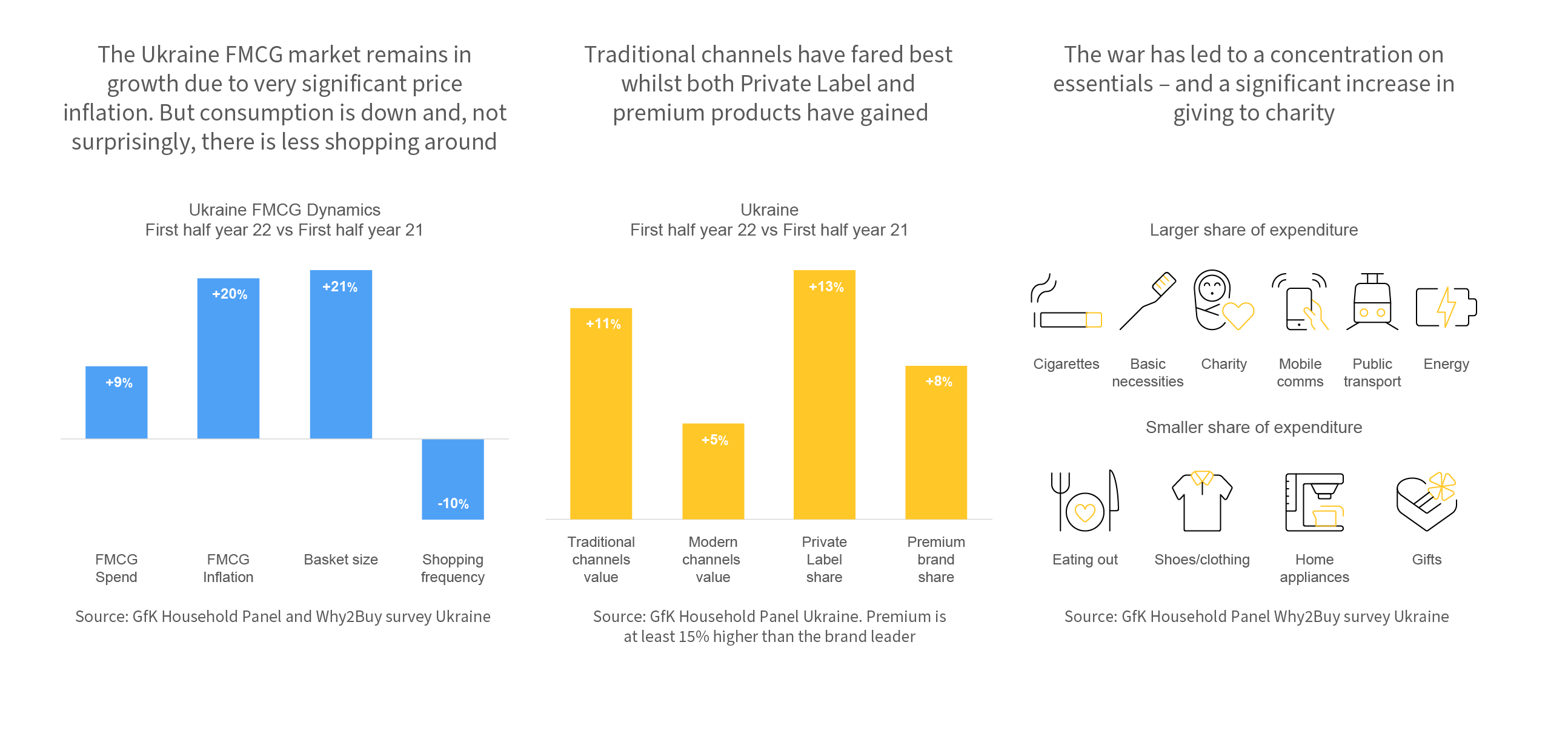

The Ukraine FMCG market remains in growth due to very significant price inflation. But consumption is down and, not surprisingly, there is less shopping around.

With the war, a rise from 4% to 14% of the population with “not enough money to cover my expenses” and the need to save money, it is not surprising that the grocery market is down in volume. But it is also very resilient when compared with pre-pandemic.

Traditional channels have fared best whilst both Private Label and premium products have gained.

Less shopping around and remaining local means that traditional rather than modern trades have increased share. The need to use resources wisely has led to more focus on price comparisons and promotions – therefore a gain in Private Label share but also, for a treat, the premium sector. There has also been more switching between brands but supply and availability are factors.

The war has led to a concentration on essentials – and a significant increase in giving to charity.

As well as basic necessities, energy and public transport are front of mind – but also mobile communications and, perhaps not surprisingly, cigarettes. And there has been a seven-fold increase in charity donations – amazing.