Small brands: More from less

Big brands are attractive for most retailers because they are able to increase shelf turnover, enjoy high equity and drawing power. Big retailers are attractive for most brands because they give them more exposure and reach more potential shoppers. However, not all retailers will feature all major brands in a category: After all, shelf space is limited, private labels also demand shelf presence and more brands add more complexity to an assortment. We examined the availability of top ten brands across more than 60 categories in the top ten retailers in 9 countries.

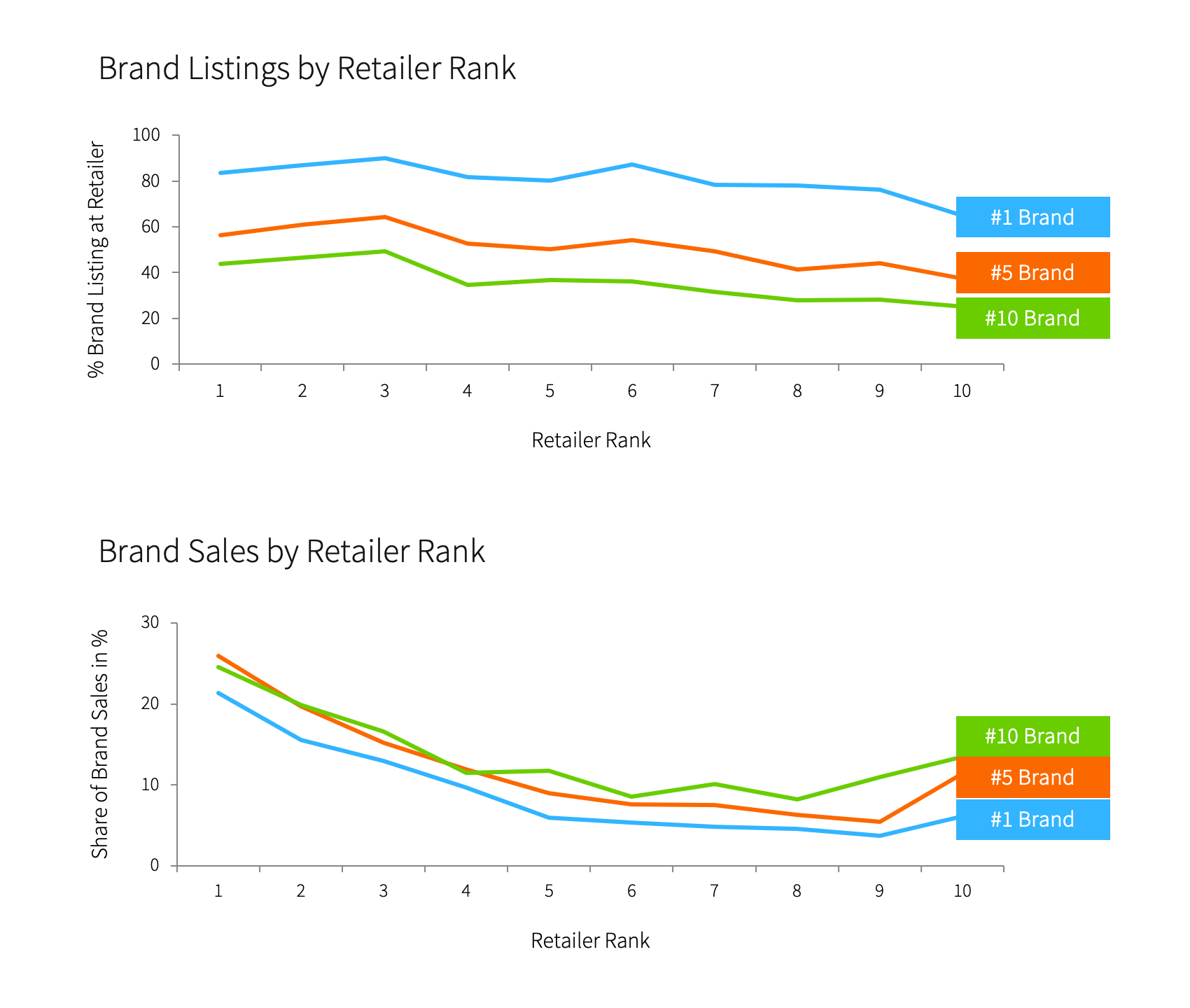

Not surprisingly, larger retailers are more likely to list brands of any rank. For example, the average number 1 brand is listed in nearly 90% of the top three retailers whereas its availability drops to below 80% in smaller retailers.

Not surprisingly, larger retailers are more likely to list brands of any rank. For example, the average number 1 brand is listed in nearly 90% of the top three retailers whereas its availability drops to below 80% in smaller retailers.- Top retailers add lower ranked brands to their assortment more often than smaller retailers do. Shoppers find the average number 6-10 brand in about half of all top three retailers, while their availability drops below 40% for smaller retailers.

- As a consequence, smaller brands rely more on each retailer where they are available. For example, number 10 brands get about one quarter of their sales from the leading retailer (when they are listed there), a level which is about 4% higher than for number 1 brands. This difference gets even more pronounced for smaller retailers with more limited assortments: The #10 retailer only captures some 5% of the typical #1 ranked brands’ sales but more than twice as much for low ranking brands.

Smaller brands do not only face buyer-based double jeopardy (fewer buyers buying them more often), but also a double jeopardy vis-à-vis retailers: They are listed by fewer retailers than bigger brands, and are more reliant on each.