PL growth over the past five years has been modest compared to the beginning of the century (only about 0.3% per year for the average category compared to 1% in the early 2000s).

What is even more reassuring for brand manufacturers: Almost 50% of categories managed to win back share from Private Labels.

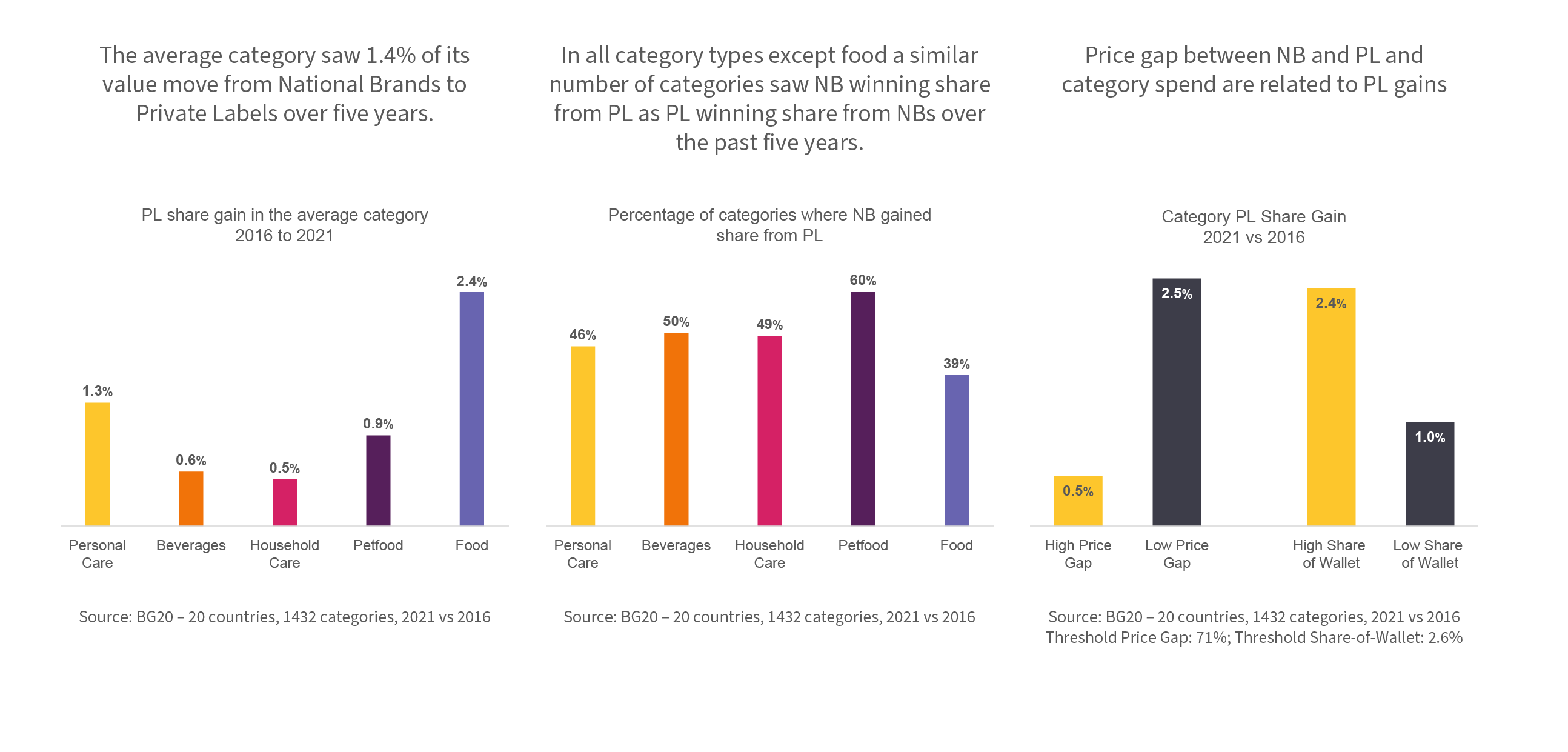

The average category saw 1.4% of its value move from National Brands to Private Labels over five years

In the average food category PL gained 2.4% share from 2016 to 2021, while the gain in the average household care and beverage category was only 0.5%.

In all category types except food a similar number of categories saw NB winning share from PL as PL winning share from NBs over the past five years

In 6 out of 10 food categories PL won share from NBs, whereas the score was more even in personal care, food and beverages. In petfood NBs gained share more often than PLs.

Price gap between NB and PL and category spend are related to PL gains

We see PL winning more share where the category accounts for a larger share of wallet (more potential to save resulting from buying PL) and where NB is relatively less expensive: People are willing to accept higher prices for brands in categories where the price premium is justified.