Comparing winning and losing brands for the period of 2018 to 2021

For many years we have been looking at behavioural metrics which distinguish winning and losing brands. This week’s edition confirms that the patterns reported earlier remain the same even in turmoil times: We compare winning and losing brands for the period of 2018 to 2021, so from a couple of years before the pandemic right into its peak.

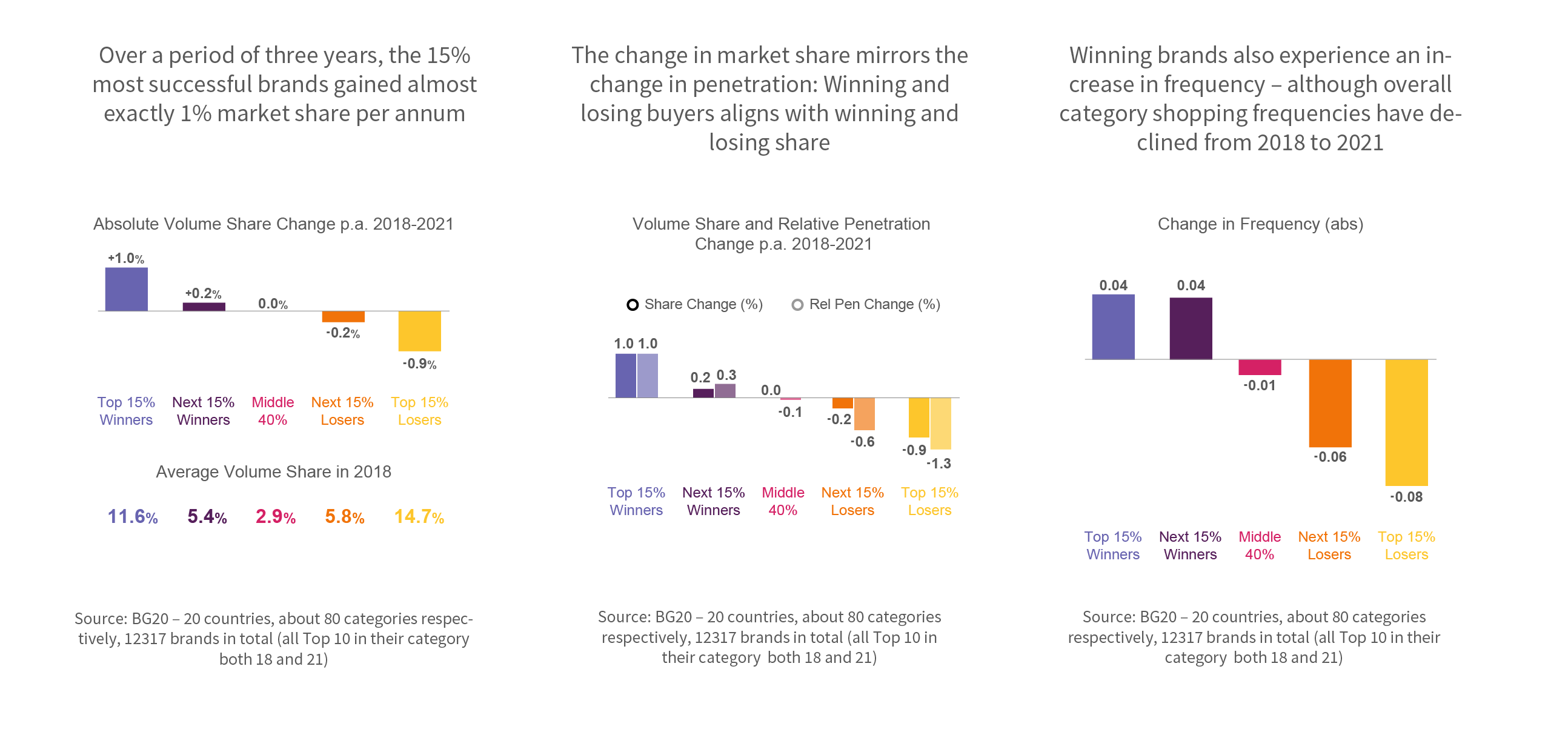

Over a period of three years, the 15% most successful brands gained almost exactly 1% market share per annum

The top tier performers have gained 1% share on average, similar to the loss of the bottom tier. The most extreme winners and losers tend to be rather large brands (those have more room to experience larger share changes) – with the winners starting out smaller than the losers in 2018.

The change in market share mirrors the change in penetration: Winning and losing buyers aligns with winning and losing share

The average share change in each of the groups strongly corresponds to the average penetration change. Is winning share possible without winning buyers? Certainly, but it’s less common: 3 out 4 share winners also increase their reach among category buyers.

Winning brands also experience an increase in frequency – although overall category shopping frequencies have declined from 2018 to 2021

During a period where the average category in our dataset has seen its frequency drop from 6.5 to 6.2 between 2018 and 2021 the most winning brands still managed to increase purchase frequency – while the losing ones, as expected, did not. The average brand in our dataset is purchased about 2.5 times per year.