Private Label growth and trade channel development

Although Private Label did not gain share in several Western European countries last year, it is growing in many other countries – hence the importance of identifying how to counter this threat to brands. Our second two articles look at trade channel development and online in particular – both showing that despite e-commerce growth, the opportunities in other channels remain sizeable and very relevant.

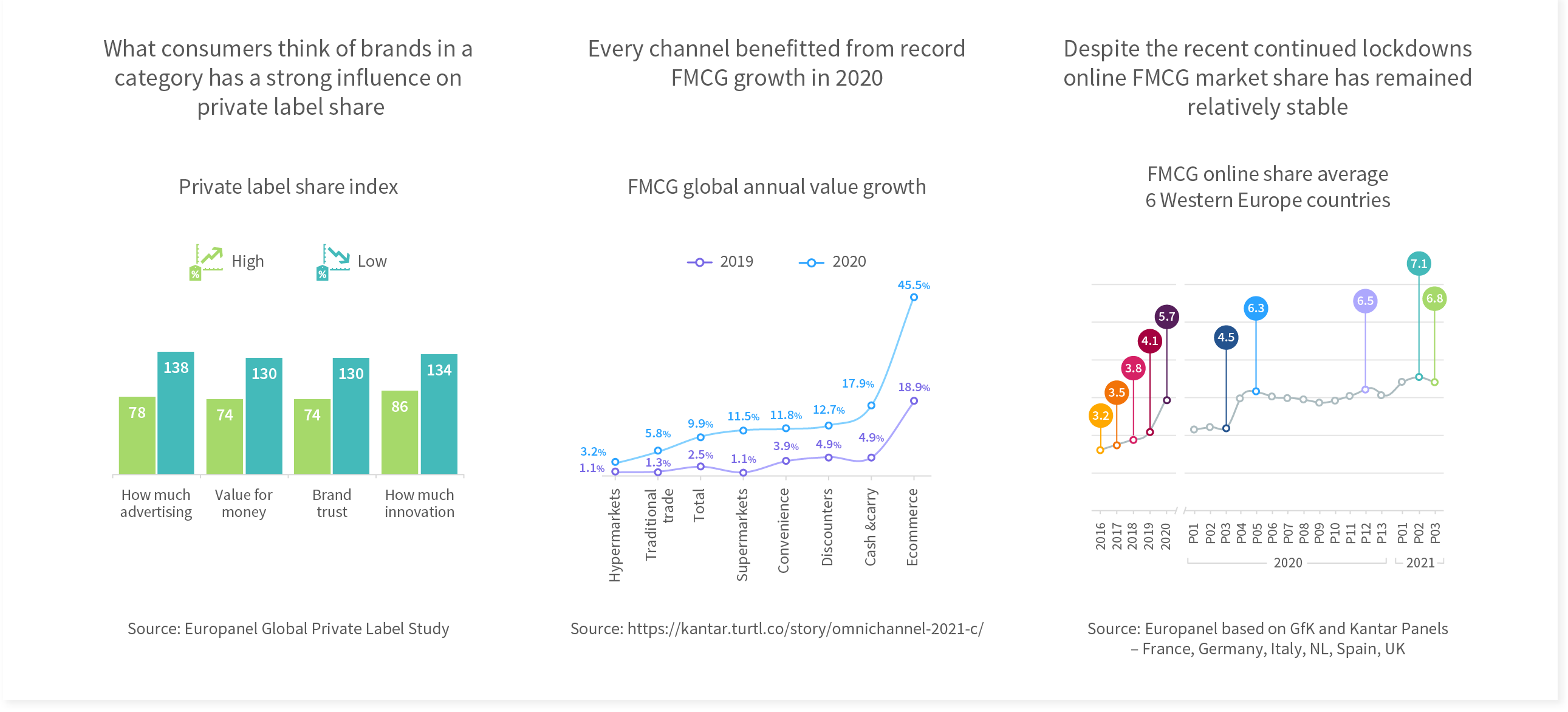

- Private Label shares are significantly lower in categories where consumers think that brands do lots of advertising, provide good value, are trusted and innovate. Maintained investment is extremely important especially in countries and categories where PL is growing.

- Of course, online showed very significant growth in 2020 but don’t forget some of the smaller proximity stores such as convenience and regular supermarkets – these could continue to profit into the future through both inertia and good experience from 2020.

- Online share peaked early in 2021 but like in 2020 this has now stabilised – now at just under 7% across the 6 countries. Remember that offline still accounts for over 90% and that older age groups, who have often driven online recently, may well return to their normal shopping routines.