1 in 3 Top 10 National Brands in a category charges more than twice the price of Private Labels.

These rather premium brands on average command a market share of 5% in terms of volume and 7.2 % in terms of value. In total, the top 10 National Brands own a share of just over 50% in the average category, slightly higher in value than volume terms.

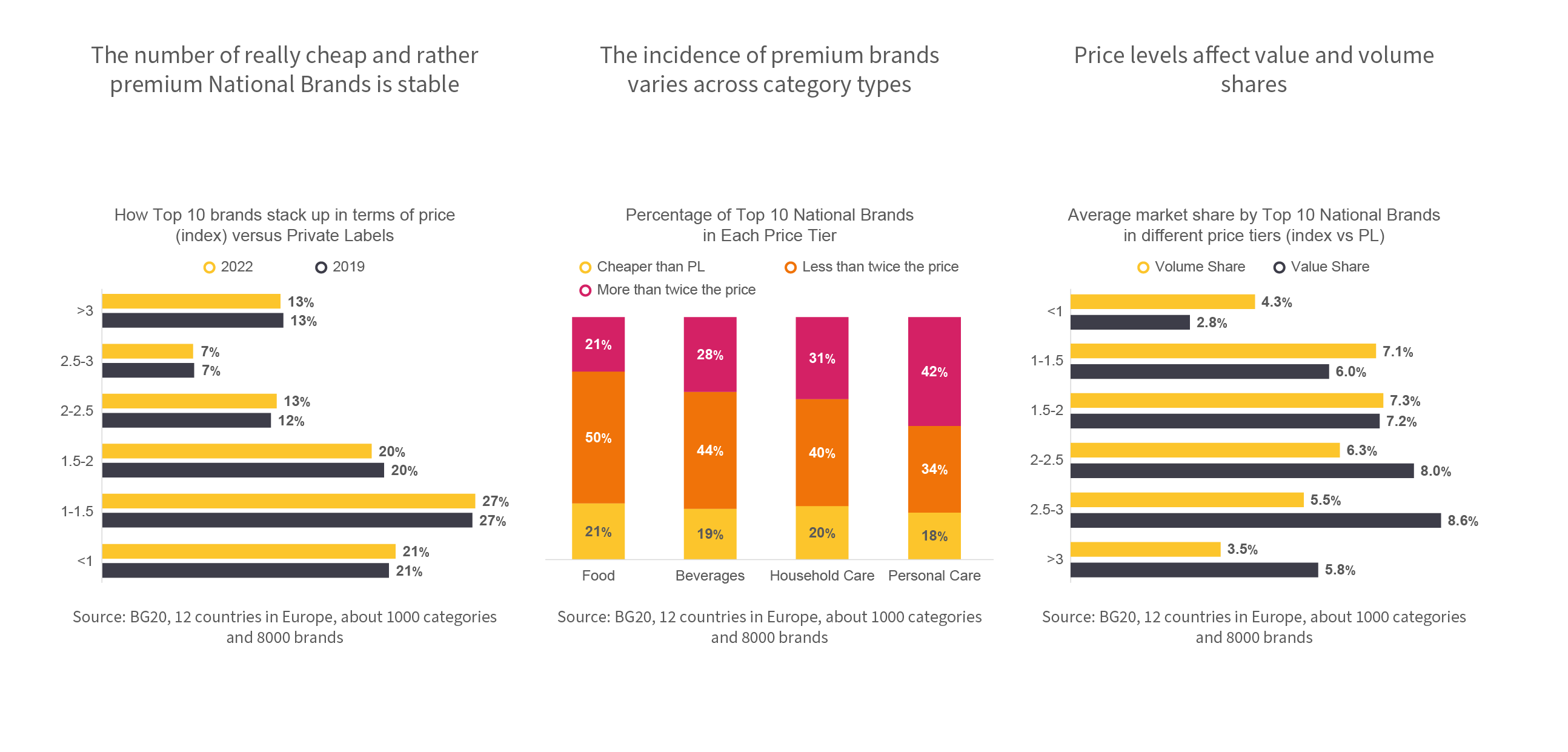

The number of really cheap and rather premium National Brands is stable

Both in 2019 and 2022 the relative number of Top 10 National Brands in different price tiers has remained very stable. 1 in 5 is cheaper than Private Labels, almost half are less than twice as expensive and one third is more than twice the price of Private Label in their category.

The incidence of premium brands varies across category types

Top 10 brands that charge more than twice the price of Private Labels are most common in Personal Care where more than 4 out of 10 Top 10 brands qualify – compared to only 2 in 10 in Food categories. Top 10 brands that charge less than Private Labels represent about 2 in 10 brands irrespective of category type.

Price level affects a brand’s value and volume share figure

While more expensive Top 10 brands are less likely to be big in terms of volume share than cheaper brands (3.5% for the most expensive tier vs. more than 7% for National Brands priced just above Private Label prices), their higher prices benefit their value shares. National Brands in the most expensive price tier (index >3) lag behind National Brands in the least expensive tier (index <1) in terms of volume share (3.5% vs 4.3%), but their value share is more than double (5.8% vs 2.8%).