Unusually high inflation has increased the importance of price in consumers’ decision-making.

This edition of Pick of the Week looks at the relative prices charged by brands in comparison to Private Labels in their category.

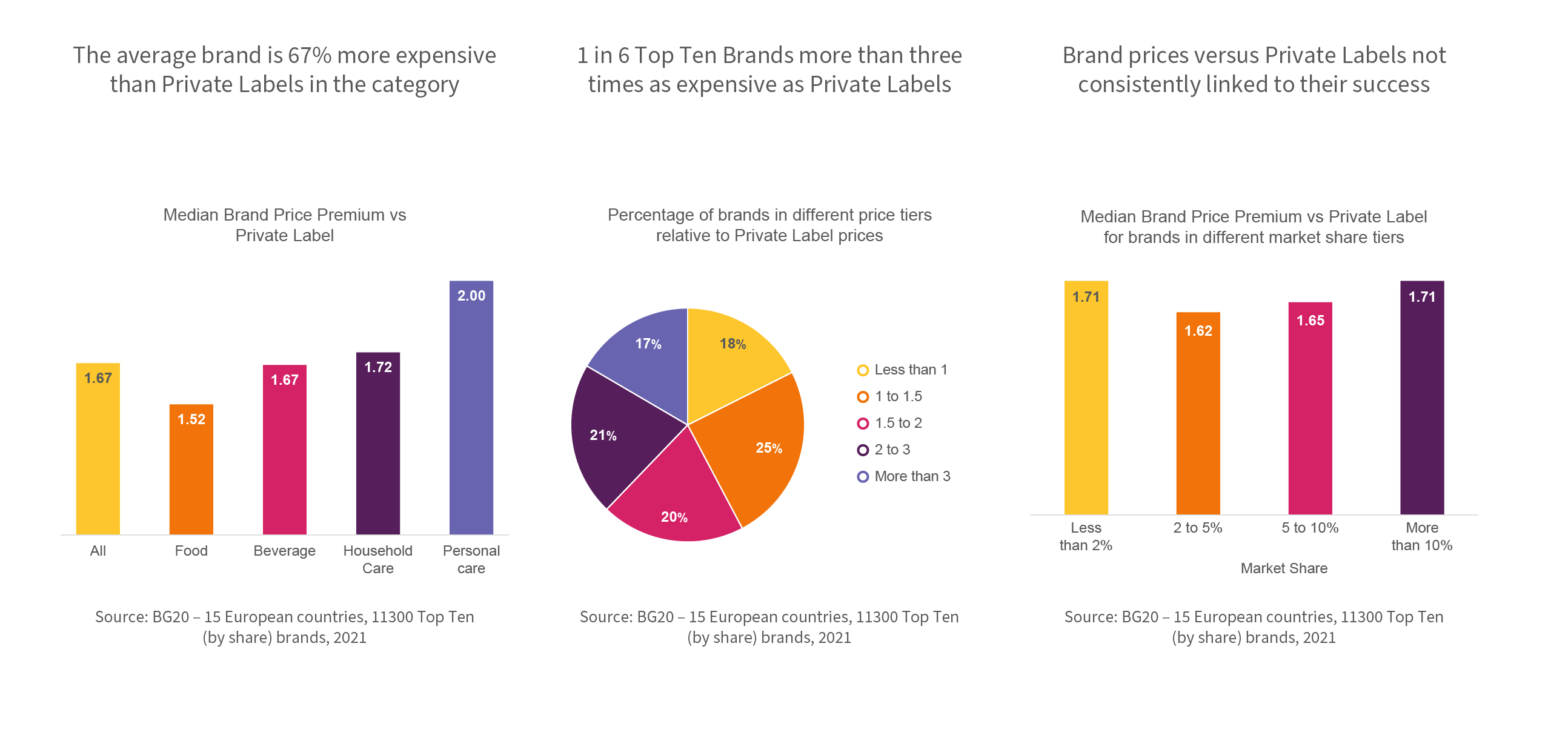

The average brand is 67% more expensive than Private Labels in the category

The price gap vs Private Label is highest in Personal Care where the average brand is twice as expensive as PL. While PL prices have increased more than brand prices lately, they do so from a lower base. Hence the absolute price distance may even have increased.

1 in 6 Top Ten Brands more than three times as expensive as Private Labels

Many brands charge a considerably higher price than Private Labels in their category. For more than one third of Top 10 brands consumers are prepared to pay twice as much or more than for the PL on offer.

Brand prices versus Private Labels not consistently linked to their success

The median price distance to Private Labels is the same for the 70% small brands (less than 2% share) in our BG20 database as for the 8% large brands (more than 10% share). Not surprisingly, however, relatively expensive brands (price ratio >3) are smaller on average than brands in less expensive price tiers.