How the same rules and drivers of growth apply to retailers as for manufacturer brands

Our first article continues the theme that the same rules and drivers of growth apply to retailers as for manufacturer brands – this week, physical presence. Our second two articles look at new product launches in 2020 – despite the pandemic, the market was extremely active in the number of introductions and in their performance.

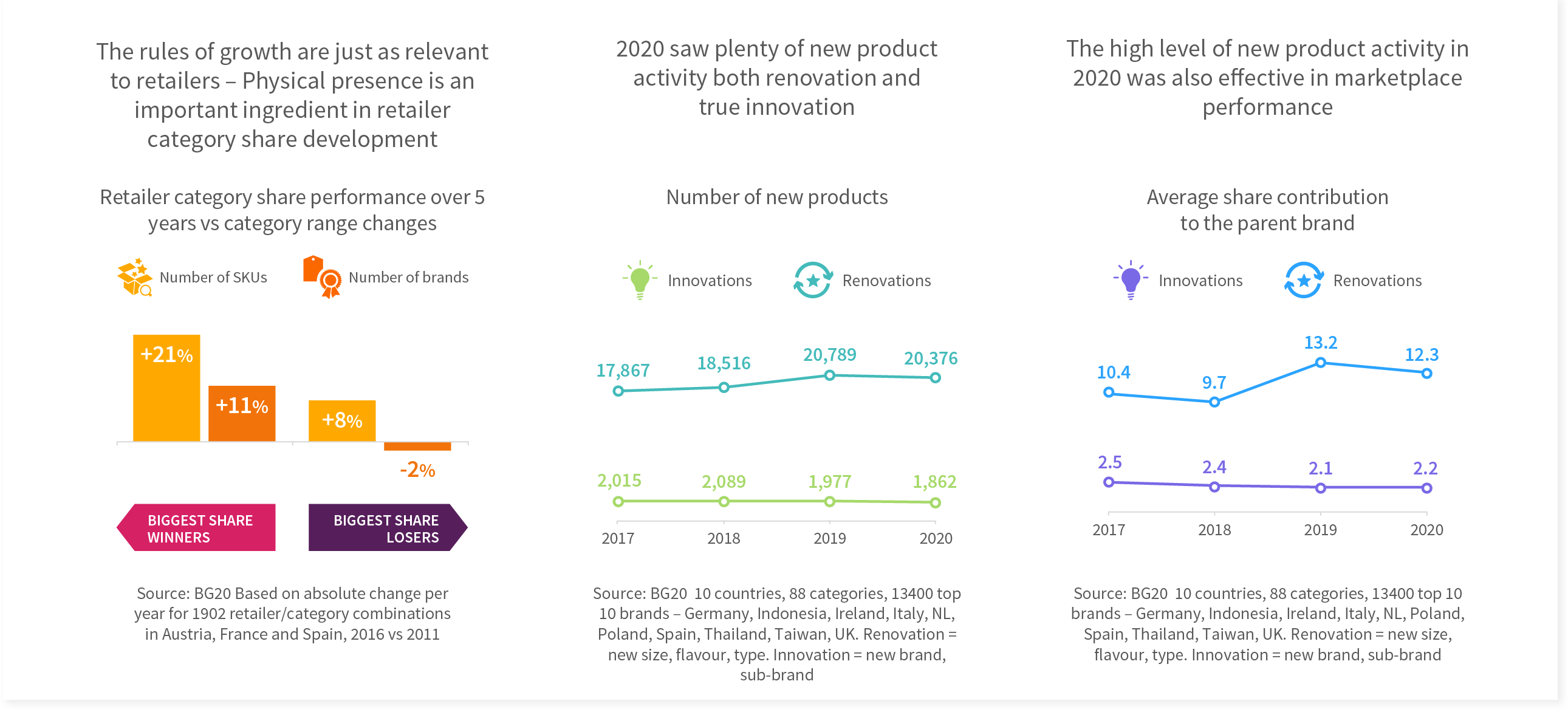

- Like for manufacturer brands, physical presence within a category is an important element in retailer share growth – the biggest share winners increased SKU count by more than double the rate of share losers – and the number of brands increased rather than decreased.

- Despite the pandemic, the scale of new product activity in 2020 showed a high level of renovation and only slightly fewer true innovations – and as published a few weeks ago, this was especially the case for brands that gained share. As always renovations dominate – 11 times more than innovations.

- Not only was NPD high in 2020, it was also translated into purchasing – the contribution to brands compared favourably with prior years – and again, it was the share winners who were the drivers. Innovations are twice as effective as renovations – 1 in 11 by number but 1 in 5.5 in contribution.