How big are the biggest brands? (Part 2)

Today we look at how a high vs a low Private Label share impacts the shares of large and small brands.

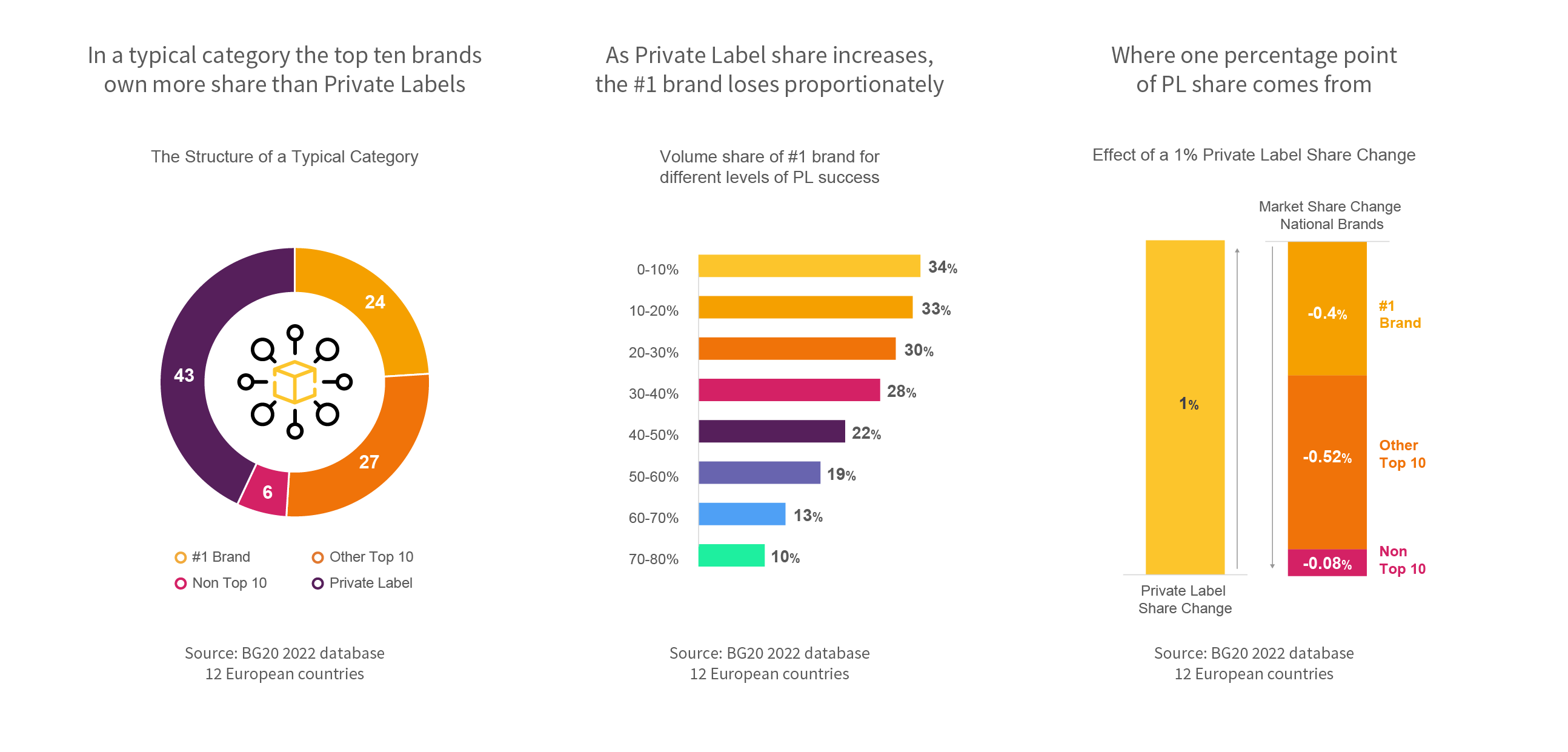

In a typical category the top ten brands own more share than Private Labels

The average #1 brand across 12 European countries sells about one quarter of the category’s volume, slightly less than the remaining top ten brands together. Private Label (aggregated across all banners) sits at about 43% and non Top Ten Brands on average play a very small role only (6%). Some categories, however, are much more fragmented – with non Top Ten brands reaching a quarter of the volume or more (think beers, spirits, or cheese in selected markets).

As Private Label share increases, the #1 brand loses proportionately

On average a 10% higher Private Label share in a category reduces the market share of the #1 brand by about 4% – almost in line with the 42% of the branded market that the #1 brand on average owns.

That decrease is less pronounced for categories where PL is rather weak (less than 40%) and more pronounced when PL has reached a considerable market share – maybe a sign that retailers prune #1 assortments and facings once their importance drops.

Where one percentage point of PL share comes from

Across many categories the contribution of a one percentage PL share difference affects different national brands as follows:

The average #1 brand loses 0.4% share (in line with its average share of the branded market of 42%).

The #2 – #10 brands jointly must expect to lose 0.52%, slightly more than expected given their 47% share of the branded market.

The non top ten brands lose 0.08%, less than expected given their 11% of the branded market – maybe a sign that retailers prune middle brands (#2 – #10) but add niche brands to signal variety.