Category effects

Over the past few weeks we have looked at inflation and impacts for product choice, store choice, total market and country. This week we look at the effects by category.

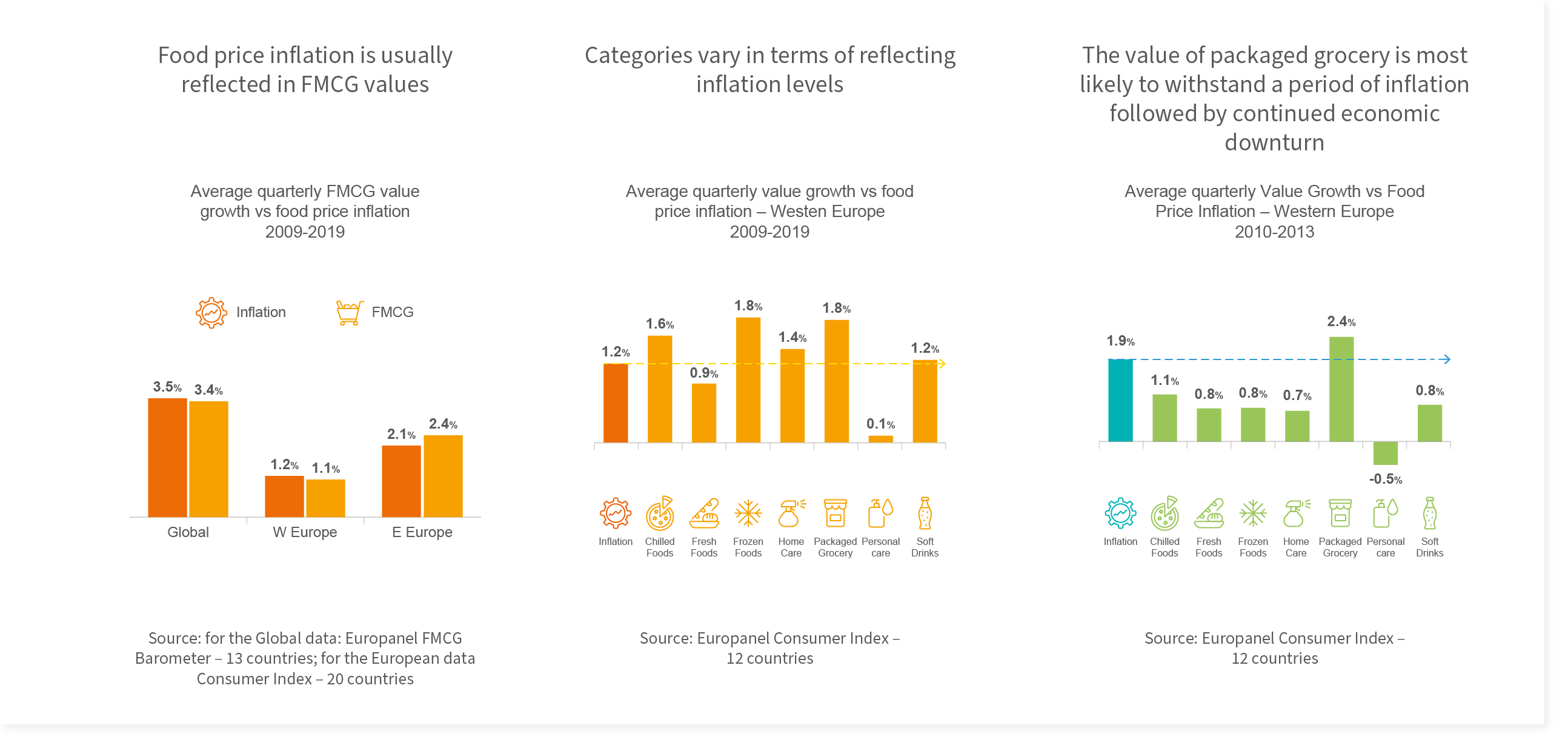

- Food price inflation is usually reflected in FMCG values

Taking the 11 years prior to the pandemic, quarterly average Food price inflation closely matched FMCG value growth due to a balance between modest volume growth and downtrading to cheaper products – downtrading was a particular feature in W Europe in the 2010-2013 economic downturn (see last week’s edition). - Categories vary in terms of reflecting inflation levels

Over the 11 years prior to the pandemic in W Europe, five of seven ‘super-categories’ were able to grow business in line or above inflation – Frozen Foods and Packaged Grocery were able to add the most value above inflation – partly volume driven as shown by individual category analyses. - The value of packaged grocery is most likely to withstand a period of inflation followed by continued economic downturn

Downtrading and stable volumes were a feature of the W European FMCG market in the 2010-2013 economic downturn. The least affected was Packaged Grocery where volumes performed better and value increased more than inflation. Trends to be aware of if the upcoming inflation spike is followed by a downturn.