Whilst inflation is having an impact on specific category purchasing

Moves to Private Label and Discounters are more general and are not focused on particular products

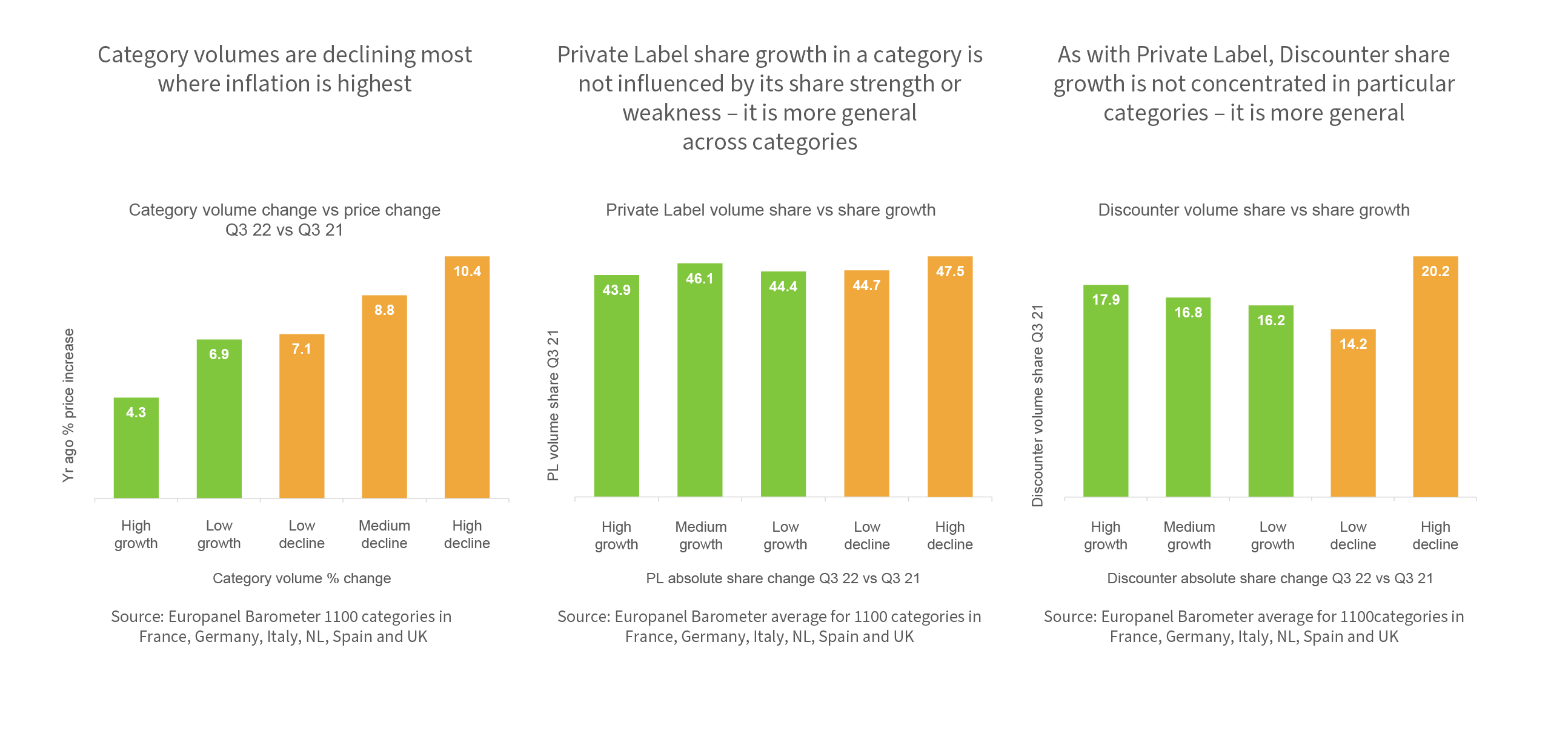

Category volumes are declining most where inflation is highest.

The average category volume remains slightly ahead of pre-pandemic. But high inflation is a key factor in year on year comparisons – especially for certain products such as oils, butter, some meats and baking.

Private Label share growth in a category is not influenced by its share strength or weakness – it is more general across categories.

PL share growth or decline by category is not related to prior PL share levels – so it is not more pronounced in categories where PL is strong or weak. There are also no specific types of product categories that show growth or decline.

As with Private Label, Discounter share growth is not concentrated in particular categories – it is more general.

As store numbers increase, Discounters are increasing share but the growth is no higher in categories where they are strong or weak, or in specific types of product categories.